Retirement planning involves coordination between income sources, tax exposure, and withdrawal timing. Each retirement phase presents distinct opportunities that influence long-term financial stability. Planning during specific periods helps retirees manage taxes and maintain income flexibility. Evaluating these timing opportunities early can support stable retirement income and clearer financial direction.

Certain stages during retirement create favorable conditions for Roth conversions. These periods often arise when taxable income temporarily declines or income sources shift. Recognizing these windows allows retirees to restructure accounts without disrupting income stability. A structured approach during these periods can improve tax efficiency and long-term retirement flexibility.

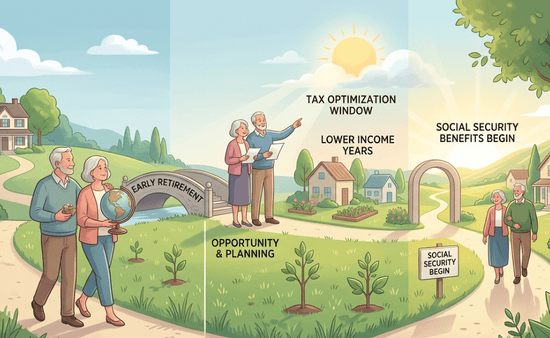

The Gap Between Retirement and Social Security Benefits

Many retirees leave employment several years before Social Security benefits begin. This transition period often results in lower taxable income compared with working years. Reduced income during this time can create a suitable opportunity for staged account conversions.

Controlled adjustments during this gap may help manage future tax obligations. This period allows changes without placing pressure on retirement withdrawals. Planning during this stage supports smoother income transitions later. This window often provides flexibility for adjustments across multiple tax years.

Temporary Low-Income Years After Leaving Employment

After retirement, income frequently declines before other benefits begin. This temporary reduction often places retirees in lower tax brackets. Lower brackets create opportunities for structured conversions at manageable tax levels. Part-time income or delayed benefit claims can extend this planning window.

Conversion activity during these years can reduce long-term taxable income. This approach supports stable retirement income preparation and improved flexibility. These years often allow retirees to make measured financial adjustments without significant tax pressure.

The Window Before Required Minimum Distributions Begin

Required minimum distributions increase taxable income once mandatory withdrawals begin. The years before this stage offer greater control over retirement account withdrawals. This flexibility allows retirees to consider conversions within favorable tax brackets.

Account adjustments before mandatory withdrawals may reduce future tax exposure. Lower balances before required distributions can support long-term tax efficiency. Planning during this window strengthens retirement income stability. This phase often allows retirees to reshape account balances before mandatory withdrawal rules apply.

Market Downturns That Reduce Retirement Account Values

Market declines sometimes reduce retirement account values temporarily. Lower valuations can create opportunities for converting assets at reduced tax cost. Conversions during these periods allow more shares moved within manageable tax ranges.

Market recovery after conversion may support tax-free growth within Roth accounts. Account adjustments during downturns can improve long-term retirement planning. Proper timing during these periods strengthens retirement income flexibility. These periods may allow retirees to reposition assets while account values remain temporarily reduced.

Before New Income Sources Such as Pensions Begin

Many retirees expect additional income from pensions or annuity payments. These new income sources can increase taxable income and limit conversion flexibility. Years before these payments begin may provide suitable conversion opportunities.

Account adjustments during this period can reduce future taxable withdrawals. This preparation helps retirees manage higher income years effectively. Proper timing before income increases supports long-term financial stability. This stage often allows retirees to prepare for consistent income changes across retirement years.

Strategic timing plays an important role in retirement account planning decisions. Each retirement phase may present favorable circumstances for structured financial adjustments. Professional guidance can help retirees identify suitable periods for Roth conversions. Planning across these windows supports consistent income, improved flexibility, and stronger retirement stability.