A first meeting with a financial advisor shapes future decisions. Clients arrive with questions about retirement and investments. They leave with either clarity or lingering confusion. The initial consultation establishes tone and mutual expectations. Both parties determine whether a productive partnership exists. Orlando residents seek advisors familiar with local economic conditions.

Financial Advisors in Orlando, FL, serve theme park employees and healthcare professionals. Aerospace engineers require equity compensation planning strategies. Small business owners need succession and key person coverage. Retirees seek sustainable withdrawal rates from accumulated assets.

The Initial Consultation Structure

Advisors ask about personal goals and timeline expectations. They inquire about current assets and income sources. Questions cover family structure and education expenses. The conversation reveals stated objectives and unspoken concerns.

Clients describe ideal retirement lifestyle and risk tolerance. Advisors explain planning philosophy and service models. Fee structures appear on printed schedule documents. Both parties assess communication styles and personal rapport.

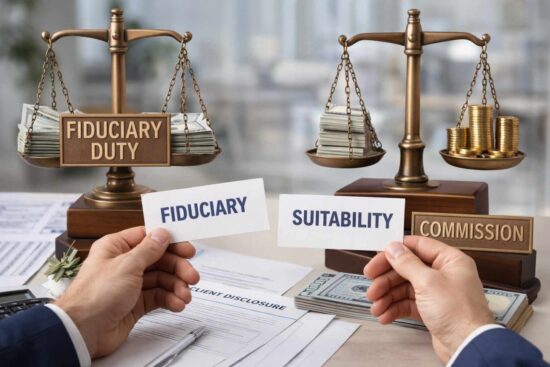

Fiduciary Duty and Compensation Models

Fee-only advisors charge transparent hourly or asset rates. Commission representatives earn payments from product providers. Hybrid models combine both compensation approaches. Clients receive disclosure documents explaining the advisor’s income.

Fiduciary advisors place client interests above compensation. Suitability standards allow conflicts with appropriate recommendations. Orlando firms operate under both regulatory frameworks. Clients ask about loyalty obligations during first meetings.

Data Collection and Goal Quantification

Advisors request tax returns and account statements. Pay stubs and pension estimates fill projection models. Current insurance policies reveal coverage gaps. Data collection spans approximately two weeks.

Net worth statements organize assets by liquidity. Cash flow analyses compare income against obligations. Goal quantification assigns dates to target figures. Retirement calculators project spending across lifespans.

Plan Presentation and Account Setup

Advisors present findings during dedicated review sessions. Charts illustrate outcomes under varying market conditions. Recommendations address investments, insurance, taxes, and when relevant, debt structure. Clients receive written summaries with priority steps.

● Investment allocation adjustments

● Insurance policy replacements

● Beneficiary designation updates

● Tax loss harvesting protocols

● Automatic contribution establishment

If real estate or refinancing plays a role in the client’s situation, advisors may also review mortgage terms—such as interest structure, amortization schedule, or payoff strategy—to ensure cash flow and long-term goals remain aligned.

Implementation begins with beneficiary and cost basis updates. Account registrations shift toward appropriate ownership structures. Automatic investment plans establish consistent contribution habits. Rebalancing protocols maintain target allocations.

Ongoing Meeting Cadence and Contact

Quarterly meetings examine portfolio performance results. Annual comprehensive reviews revisit goals and statements. Life events trigger immediate schedule adjustments. Marriage and job changes require plan modifications.

Client portals provide continuous account access. Advisors respond to emails within one business day. Market commentary arrives during unusual volatility. The relationship evolves from transactional to consultative.

How to Identify Qualified Financial Experts?

Professional designations indicate advanced training beyond basic licenses. Certified Financial Planner marks completion of rigorous coursework and examination. Certified Public Accountant credentials verify tax and accounting expertise. Chartered Financial Consultant designations focus on insurance and estate planning.

Local bar associations maintain referral lists for attorney collaborations. Professional networks connect families with credentialed practitioners. Orlando firms display team credentials prominently on websites. Prospective clients verify designations through independent certifying body databases.

Financial Advisors in Orlando, FL, guide clients through accumulation and distribution. The partnership begins with honest fee discussions. Data transforms into actionable planning scenarios. Regular reviews maintain alignment with original goals. Trust develops through consistent competence and communication. The relationship measures success through client confidence.